Vacation Home- The Ultimate Hideaway

If a mountain getaway or an ocean view has become your American dream, then perhaps you should know a vacation home can still offer some tax savings that will help pay for your hideaway. The rules have changed though, and they differ depending on whether you use the home solely for enjoyment or mix business with pleasure by renting the property part-time.

You can deduct all of the interest paid on a mortgage used to buy a second home as long as the combined debt secured by the vacation home and your principal residence does not exceed $1 million. This advantage is restricted to two homes. If you purchase a third, interest on that mortgage is non-deductible. However, no matter how many homes you have, you may be able to deduct all the property taxes you pay.

One break enjoyed by homeowners – the right to immediately deduct points paid on a mortgage – applies only to a principal residence. Points paid a loan for a vacation home must be deducted gradually as you pay off the mortgage.

Personal Residence

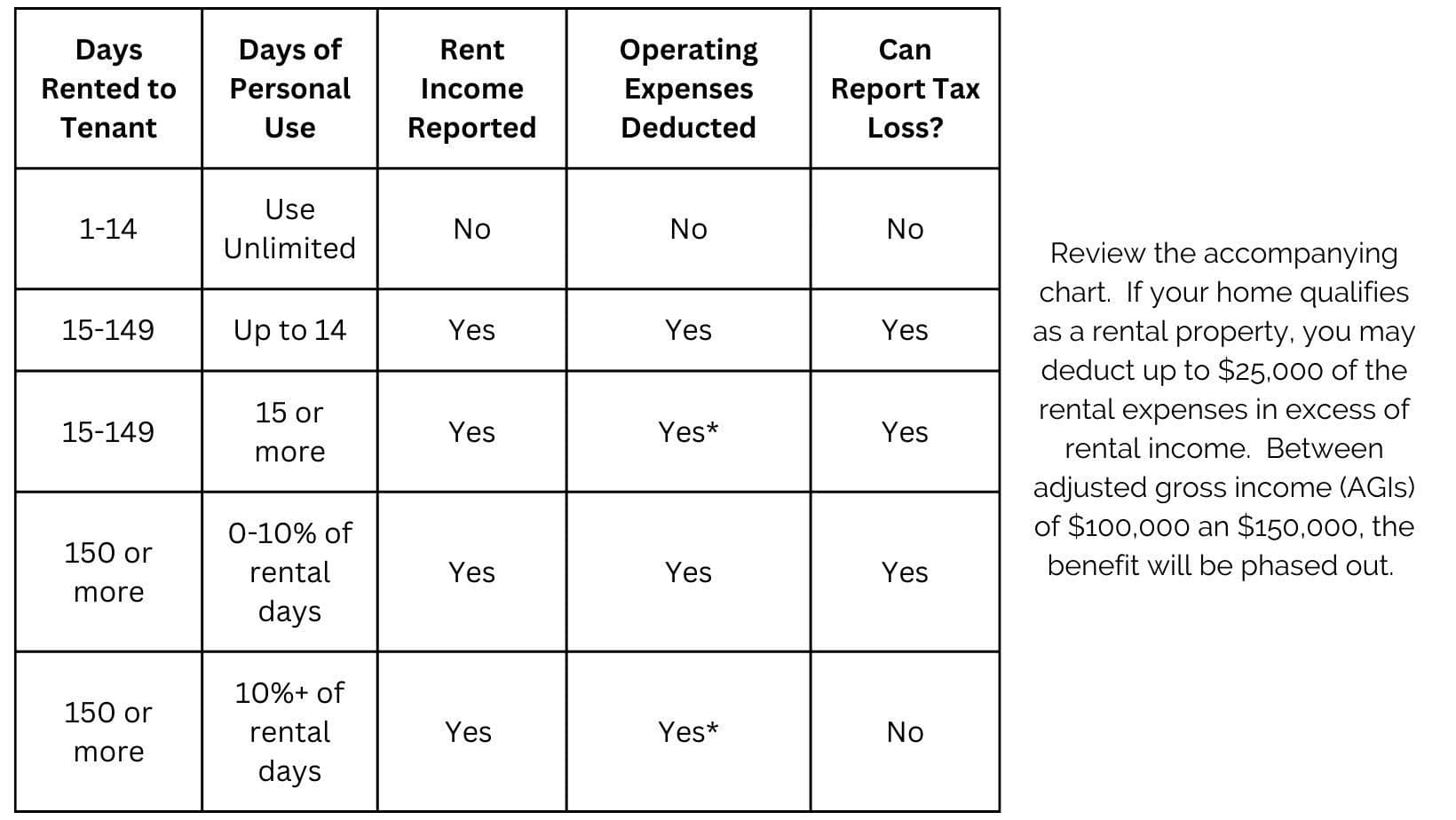

Your vacation home counts as a personal residence even if you rent it for up to 14 days a year. In that case, you get to retain the rent tax-free and don’t jeopardize your mortgage interest and tax deductions. If you rent out the house on a continual basis, things may become complicated. Different rules apply depending on the breakdown between personal and rental use.

First, if you buy primarily for pleasure but rent for 15 days or more, the rent you receive is taxable. The house is still considered a personal residence though, so you get to deduct all the interest and property taxes. You may also be able to deduct all other expenses including the cost of utilities, repairs, and insurance attributable to the time the house is rented. In some cases, you might even get to deduct depreciation. When the house is considered a personal residence, rental deductions can’t exceed the amount of rental income you report. In other words, your second home can’t produce a tax loss to shelter other income. In most cases, the interest and taxes assigned to the rental use of the house, plus the operating expenses, more than offset the rental income, giving you no chance to write off depreciation.

Rental Property

Now consider your tax situation if you buy a property primarily as an investment and limit your personal use of the property to 14 days a year (or 10%of the number of rental days it allows you more than 14). The house is a rental property in the eyes of the Internal Revenue Service (IRS), so your deductions can exceed the amount of rental income you receive. That opens the door to depreciation write-offs which, in the past, could produce big paper losses and big tax savings. The advantage to you, though, depends on whether you’re affected by the “passive loss” rules.Basically, rental losses are classified as passive and can be deducted only against passive income from another rental property or a limited partnership. If you do not have passive income to shelter, the losses have no immediate value (unused losses can be used in future years when you have passive income).

There’s an exception to this rule, how ever, that permits taxpayers with adjusted gross income (AGI) under $100,000 to deduct up to $25,000 ($12,500 if married, filing a separate return, and lived apart from a spouse for the entire tax year) of passive losses against other kinds of income including salaries. To qualify, you have to actively manage the property. The $25,000 allowance is gradually phased out as AGI rises between $100,000 and $150,000.When your vacation home is really a rental property, the mortgage interest attributable to the time the premises are rented is a business deduction. The rest, though, can’t be deducted as home mortgage interest since the house doesn’t qualify as a personal residence. Whether tax deductible or not, the expenses you incur for a vacation home should come second to the enjoyment you will derive from using the vacation home. Depending on the location and the desirability of the property, it often can be financially rewarding proposition.

One break enjoyed by homeowners – the right to immediately deduct points paid on a mortgage – applies only to a principal residence. Points paid a loan for a vacation home must be deducted gradually as you pay off the mortgage.

Personal Residence

Your vacation home counts as a personal residence even if you rent it for up to 14 days a year. In that case, you get to retain the rent tax-free and don’t jeopardize your mortgage interest and tax deductions. If you rent out the house on a continual basis, things may become complicated. Different rules apply depending on the breakdown between personal and rental use.

First, if you buy primarily for pleasure but rent for 15 days or more, the rent you receive is taxable. The house is still considered a personal residence though, so you get to deduct all the interest and property taxes. You may also be able to deduct all other expenses including the cost of utilities, repairs, and insurance attributable to the time the house is rented. In some cases, you might even get to deduct depreciation. When the house is considered a personal residence, rental deductions can’t exceed the amount of rental income you report. In other words, your second home can’t produce a tax loss to shelter other income. In most cases, the interest and taxes assigned to the rental use of the house, plus the operating expenses, more than offset the rental income, giving you no chance to write off depreciation.

Rental Property

Now consider your tax situation if you buy a property primarily as an investment and limit your personal use of the property to 14 days a year (or 10%of the number of rental days it allows you more than 14). The house is a rental property in the eyes of the Internal Revenue Service (IRS), so your deductions can exceed the amount of rental income you receive. That opens the door to depreciation write-offs which, in the past, could produce big paper losses and big tax savings. The advantage to you, though, depends on whether you’re affected by the “passive loss” rules.Basically, rental losses are classified as passive and can be deducted only against passive income from another rental property or a limited partnership. If you do not have passive income to shelter, the losses have no immediate value (unused losses can be used in future years when you have passive income).

There’s an exception to this rule, how ever, that permits taxpayers with adjusted gross income (AGI) under $100,000 to deduct up to $25,000 ($12,500 if married, filing a separate return, and lived apart from a spouse for the entire tax year) of passive losses against other kinds of income including salaries. To qualify, you have to actively manage the property. The $25,000 allowance is gradually phased out as AGI rises between $100,000 and $150,000.When your vacation home is really a rental property, the mortgage interest attributable to the time the premises are rented is a business deduction. The rest, though, can’t be deducted as home mortgage interest since the house doesn’t qualify as a personal residence. Whether tax deductible or not, the expenses you incur for a vacation home should come second to the enjoyment you will derive from using the vacation home. Depending on the location and the desirability of the property, it often can be financially rewarding proposition.

Mortgage interest and property taxes are included in the deductions subject to phase out.

Deductions for points must be spread over the life of the loan.*Up to rental income.

There are other tax-cutting strategies in addition to those mentioned here. If you would like assistance in selecting tax-saving strategies that make the most sense in your situation, contact us today!